How FinTech Apps Can Improve User Retention

Author

Vignesh

Published On

You spent months maybe years building your FinTech product. You raised capital, assembled a team, survived a grueling launch, and watched your user numbers climb. Then something quietly started happening: the growth graph flattened. Users were signing up, completing onboarding, and then disappearing.

This is the silent crisis inside FinTech today. Acquisition is no longer the primary growth bottleneck retention is. And at the center of nearly every retention failure is the same root cause: a user experience that was never truly designed for the people who have to live with it.

This guide is written for FinTech founders, product managers, and technology leaders who are serious about turning their apps into products users genuinely want to return to. You will find actionable UX strategies, the metrics that matter, and a clear picture of what strong retention actually does for your bottom line.

Why User Retention Is the Biggest Growth Challenge for FinTech Apps

Across the FinTech landscape, companies are running an expensive and unsustainable race: pour money into marketing, acquire users, watch them leave, repeat. This cycle is not just inefficient it is strategically dangerous.

Here is the economic reality most founders understand too late. Acquiring a new FinTech customer costs five to seven times more than retaining an existing one. A 5% improvement in retention rates can increase overall profitability by 25 to 95%, according to research from Bain & Company. In a sector where trust, regulatory friction, and switching costs are high, your existing users represent your most valuable and underutilized growth asset.

The FinTech category is also uniquely vulnerable to retention failure because users bring deep anxieties about money, security, and complexity into every interaction. Unlike a social media app where a bad session is a minor inconvenience, a confusing banking experience or a failed payment creates lasting distrust that is almost impossible to reverse.

The companies winning in FinTech whether that is a neobank, a wealth management platform, a payments startup, or a lending app share a defining characteristic: they have built retention into the DNA of their product experience.

Common Reasons Users Stop Using FinTech Applications

Before designing for retention, you need to understand the specific forces driving your users away. Based on patterns observed across hundreds of FinTech product audits and user research studies, the most common departure triggers fall into these categories:

Friction-Heavy Onboarding and KYC Processes

The industry average for onboarding completion in FinTech hovers around 40 to 60%, meaning roughly half of all users who start the signup process never finish it. Multi-step KYC verification, document upload requirements, and poor error handling create frustration before users experience a single moment of value.

Lack of Perceived Value Early in the Journey

If a user cannot identify what your app genuinely does for them within the first two to three sessions, they have no rational reason to return. Many FinTech apps front-load complexity account setup, verification, terms and conditions and delay value delivery until users have already lost interest.

Poor Dashboard Design and Confusing Navigation

Financial data is inherently complex. When users cannot quickly locate balances, transaction history, or key features, they experience cognitive fatigue. In a trust-sensitive category like FinTech, confusion is not just annoying it erodes confidence.

Irrelevant or Excessive Notifications

Notification fatigue is a documented retention killer. When users receive generic, poorly timed, or irrelevant push notifications, 68% of them either disable notifications entirely or uninstall the app. Notifications are one of the most powerful re-engagement tools available when they are used intelligently.

Security Concerns and Low Trust Signals

Users handle their financial lives inside FinTech apps. Any interface element that feels insecure, dated, or amateurish triggers subconscious alarm signals. Trust is not established once during onboarding it must be continuously reinforced across every interaction.

One-Size-Fits-All Product Experiences

A university student using a budgeting app has completely different goals from a small business owner managing invoices. When FinTech products fail to adapt to user context and needs, engagement inevitably collapses. Personalization is no longer a premium feature it is a baseline retention requirement.

Why UX Design Plays a Critical Role in FinTech Retention

There is a persistent misconception in the FinTech industry that retention is primarily solved by features, pricing, or integrations. The data consistently tells a different story.

According to Forrester Research, every dollar invested in UX returns between $2 and $100. Users who rate their experience with a FinTech app as "very easy" are 6 times more likely to recommend it to others and 4 times more likely to use additional products. In a category where word-of-mouth drives some of the highest-quality acquisitions, this compounding effect is transformative.

UX design in FinTech is not about making something look attractive. It is about reducing cognitive load so users can make financial decisions with clarity. It is about building trust through visual hierarchy, information architecture, and consistent interaction design. It is about designing emotional experiences that make users feel confident, informed, and in control of their financial lives.

When UX is treated as a strategic business function not a cosmetic layer applied at the end of development it becomes one of the most powerful retention levers available to your product team.

10 UX Strategies FinTech Apps Use to Improve User Retention

1. Simplify User Onboarding

The first session is the most important session your product will ever deliver. Every second of unnecessary friction during onboarding is a conversion problem, a retention problem, and a revenue problem.

High-performing FinTech apps approach onboarding as a progressive experience. Rather than demanding all information upfront, they deliver immediate value a dashboard preview, a quick balance overview, a sample transaction and collect user information incrementally as trust is established. The goal is to compress time-to-value to under three minutes.

Proven onboarding tactics that measurably improve FinTech retention include:

Progressive profiling collect only the minimum viable information at signup

Welcome sequences that explain one core value proposition per screen

Clear progress indicators so users know exactly where they are in the process

Contextual tooltips that activate on first use of a key feature, not during setup

Social proof elements user counts, reviews, security badges placed at friction points

2. Reduce Friction in KYC Verification

Know Your Customer verification is a regulatory requirement in most FinTech categories, but how it is designed has an enormous impact on both completion rates and first impressions. Every unnecessary step, every poorly worded error message, and every document upload that fails silently costs you users who will never return.

Best-in-class FinTech KYC experiences share several design principles: they use AI-powered document scanning to reduce manual entry, they provide real-time feedback on document quality before submission, they offer clear explanations of why each piece of information is required, and they design compassionate error states that guide users toward resolution rather than abandoning the process.

A well-designed KYC flow can improve completion rates by 30 to 50% one of the highest-ROI improvements available in early-stage FinTech product development.

3. Design Trust Into Every Interaction

Trust in financial products is not a feeling it is a design outcome. It is built through micro-decisions that accumulate across hundreds of interactions: the precision of your typography, the responsiveness of your transitions, the clarity of your error messages, the consistency of your security indicators.

Trust-forward design in FinTech means displaying security certifications prominently without making the app feel like a compliance document. It means using plain language for financial terms so users feel informed rather than confused. It means designing transaction confirmations that feel deliberate and final. And it means building undo flows and support access into sensitive actions so users feel protected rather than exposed.

In FinTech, trust is your most renewable competitive resource. Every design decision either deposits into or withdraws from your user's trust account.

4. Personalize User Experiences

Generic experiences produce generic engagement. The FinTech apps with the highest long-term retention rates are those that adapt their interface, content, and recommendations based on individual user behavior, goals, and financial context.

Personalization in FinTech does not require sophisticated machine learning at launch. It begins with simple behavioral signals: the features a user accesses most frequently, the transaction categories that dominate their history, the times of day they engage with the app. Using these signals to surface relevant information, tailor the dashboard layout, and prioritize features creates an experience that feels built for the individual user rather than designed for a statistical average.

As data accumulates, more advanced personalization becomes available: proactive financial insights, contextualized product recommendations, and dynamically adjusted risk communications.

5. Create Financial Education Moments

One of the most underutilized retention strategies in FinTech is financial literacy design embedding education directly into the product experience at moments of relevant context. When a user receives a transaction, that is an opportunity to explain a fee. When a savings milestone is reached, that is an opportunity to introduce an investment concept. When a credit score changes, that is an opportunity to explain why.

Financial education moments serve two retention functions simultaneously. They increase product engagement by creating genuine value beyond the transactional. And they reduce user anxiety by making the financial world feel navigable rather than opaque. Users who feel financially empowered by your app are dramatically more likely to return and to expand their use of your product.

6. Use Smart Notifications Instead of More Notifications

The difference between a re-engagement notification and an uninstall trigger is relevance and timing. Most FinTech apps send too many notifications of too little value and users respond by disabling them entirely.

Smart notification design in FinTech is built on three principles: contextual relevance (the notification connects to something the user actually cares about), behavioral timing (the notification arrives when the user is most likely to act on it based on historical patterns), and clear value (the notification answers the question "why should I open this right now" before the user even taps).

When notification strategy is rebuilt around these principles, open rates typically improve by 40 to 60%, and re-engagement from dormant users increases significantly. Notifications become a retention asset rather than a churn accelerator.

7. Introduce Gamification and Rewards

Behavioral psychology has a long history of application in consumer technology, and FinTech is one of the categories where it translates most powerfully. Savings streaks, spending milestones, cashback rewards, referral programs, and achievement badges all activate the same neurological reward pathways that drive engagement in gaming and social media.

The most effective FinTech gamification is purpose-aligned: it rewards behaviors that are genuinely in the user's financial interest. A savings streak that rewards consistent deposit behavior improves both user engagement and financial outcomes simultaneously, creating a product experience that users associate with positive life progress.

The key design constraint is authenticity gamification must feel like a natural extension of the financial experience rather than a layer of superficial novelty layered on top of a functional product.

8. Use AI to Deliver Better Financial Experiences

Artificial intelligence is transforming what is possible in FinTech UX. AI-powered features that directly impact retention include: personalized spending analysis that surfaces insights users would never find independently, predictive cash flow modeling that warns users of upcoming balance issues before they become problems, intelligent search that understands natural language queries about account history, and automated categorization that reduces the manual work users typically associate with financial management.

AI also enables a fundamentally new kind of user assistance: conversational interfaces that can answer nuanced financial questions, guide users through complex decisions, and surface support options without requiring users to navigate help documentation. Products that get AI assistance right see measurable improvements in both task completion rates and user satisfaction scores.

9. Continuously Optimize Through User Feedback

Retention improvement is not a one-time design sprint it is an ongoing organizational practice. The most resilient FinTech products have built feedback collection and analysis into their product development lifecycle at every stage.

This means embedding in-app feedback mechanisms at key moments immediately after task completion, following a support interaction, upon reaching a financial milestone. It means running regular usability testing sessions with representative users, not just internal team members. And it means treating quantitative signals session length, feature adoption, drop-off points and qualitative signals support tickets, app reviews, user interviews as a unified picture of experience quality.

The FinTech companies that consistently win on retention are those that treat every piece of negative user feedback as a product roadmap input rather than a customer service problem.

10. Improve Dashboard Usability and Navigation

The dashboard is the heartbeat of any FinTech application. It is the screen users return to most often, the primary surface on which financial confidence is either built or eroded, and the navigation hub through which all other features are discovered.

High-retention FinTech dashboards share a set of design characteristics: they surface the most personally relevant financial information immediately without requiring navigation, they use clear visual hierarchy to distinguish between primary metrics and supporting detail, they provide contextual quick actions that anticipate what the user is likely to do next, and they maintain consistent navigation patterns so users never have to think about where to find what they need.

Dashboard usability audits frequently reveal significant retention opportunities. Small improvements in information architecture and navigational clarity can produce measurable increases in session frequency and depth of feature engagement.

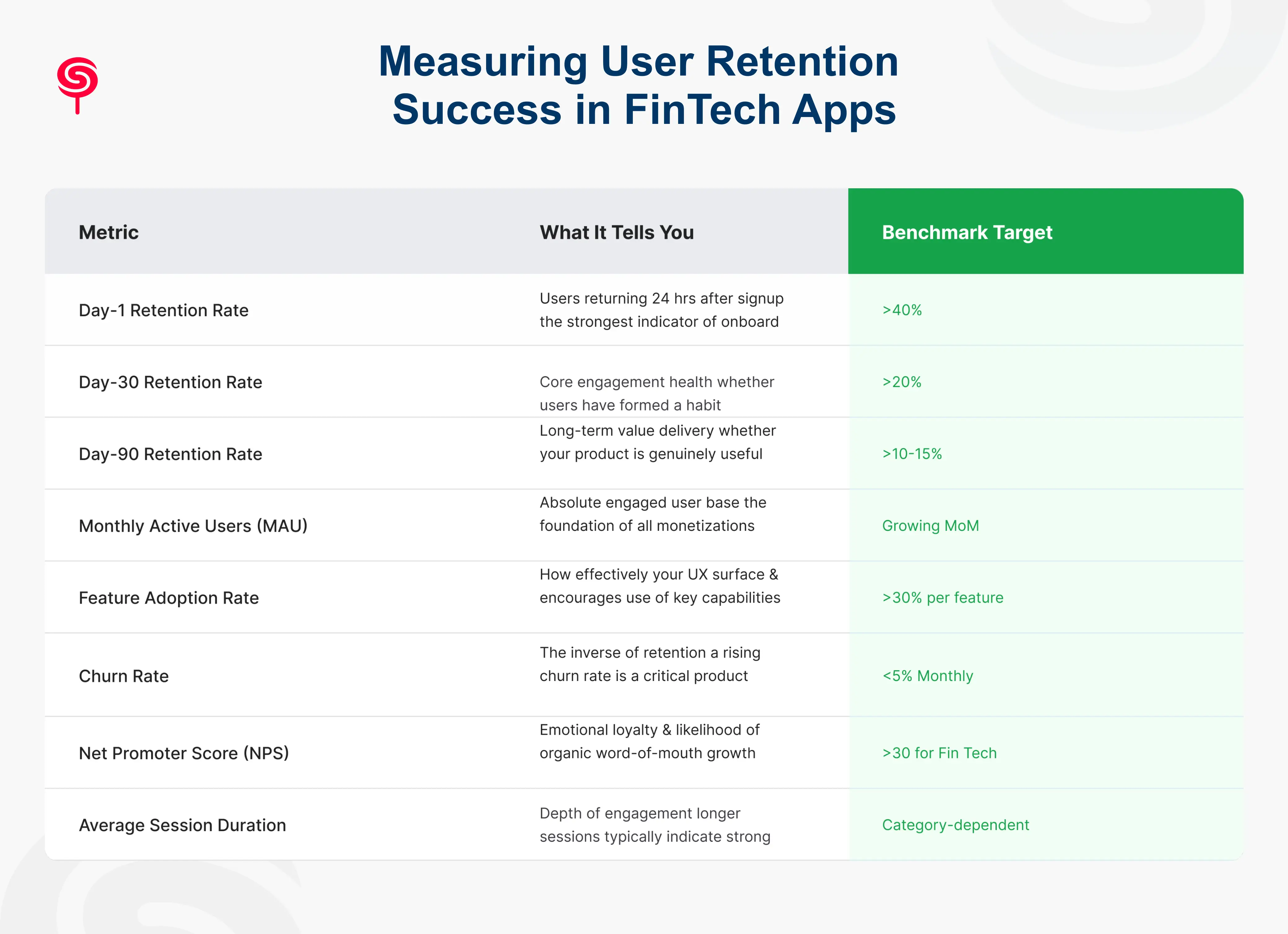

Measuring User Retention Success in FinTech Apps

Improving retention requires knowing precisely how to measure it. The metrics that matter most in FinTech user retention analysis are:

Business Outcomes of Strong FinTech User Retention

The case for investing in UX as a retention strategy is not simply philosophical it is quantifiable across every key business metric. When FinTech products significantly improve user retention, the downstream business effects are compounding and measurable:

Higher Customer Lifetime Value

Retained users engage with more product features, convert on premium offerings, and generate higher transaction volumes over time. A user retained for 12 months versus 3 months typically generates 4 to 7 times the revenue. LTV is the most important unit economics metric in FinTech, and retention is its primary driver.

Lower Customer Acquisition Cost Efficiency

When you stop hemorrhaging users at the 30 and 90-day marks, the economics of your acquisition spending improve dramatically. The same marketing budget that previously replaced churned users now drives net growth. This is the flywheel effect that separates FinTech companies that scale profitably from those that grow while losing money.

Stronger Word-of-Mouth and Organic Growth

Retained users become advocates. In financial services where trust is the primary purchase driver a referral from a trusted peer is worth exponentially more than any paid acquisition channel. High-retention FinTech products consistently report that organic and word-of-mouth acquisition grows as a percentage of total acquisition over time.

Better Regulatory and Investor Positioning

Retention metrics are increasingly scrutinized by both investors and regulators as indicators of product health and sustainable business practice. High Day-30 and Day-90 retention rates demonstrate product-market fit in a way that raw user numbers cannot. For fundraising and strategic partnership conversations, retention data is one of your most persuasive assets.

How a UX Audit Can Identify Retention Gaps in Your FinTech Product

The majority of FinTech retention problems are invisible to internal teams because they exist inside the lived user experience in the hesitations, confusions, and frustrations that users encounter but rarely report directly. A professional UX audit is designed to surface these hidden failure points before they become churn statistics.

What a FinTech UX Audit Examines

A comprehensive UX audit for a FinTech product typically evaluates the following areas:

Onboarding funnel analysis where users drop off and why

KYC flow usability completion rates and friction point identification

Information architecture review whether users can find what they need without thinking

Dashboard and navigation heuristic evaluation applying established UX principles to identify design violations

Trust and security signal assessment whether the interface communicates safety effectively

Notification strategy review relevance, timing, and engagement rate analysis

Accessibility compliance whether the product is usable by all financial consumers

Competitive experience benchmarking how your UX compares to best-in-class FinTech products

What a UX Audit Delivers

The output of a rigorous FinTech UX audit is not a list of opinions about design. It is a prioritized, evidence-based retention improvement roadmap. Each finding is mapped to its estimated impact on specific retention metrics, allowing your product team to sequence improvements for maximum ROI.

For most FinTech products, a UX audit identifies enough improvement opportunities to meaningfully move retention metrics within one or two product development cycles often without requiring new features, additional engineering resources, or changes to core functionality.

The question for most FinTech founders and product leaders is not whether a UX audit would surface actionable retention insights. It is how much revenue is being lost each month without one.

Conclusion

User retention in FinTech is not a marketing challenge, a pricing challenge, or a competitive challenge. It is a design challenge. The apps that users return to consistently the ones that become trusted financial companions rather than forgotten installs are products where every interaction has been deliberately designed to deliver clarity, build trust, and create genuine value.

The 10 UX strategies outlined in this guide are not abstract best practices. They are proven retention levers that FinTech companies across neobanking, payments, wealth management, and lending have used to measurably reduce churn, increase lifetime value, and build the kind of product loyalty that compounds into sustainable competitive advantage.

If you are serious about improving retention in your FinTech product, the place to begin is with an honest assessment of where your user experience is creating friction, eroding trust, or failing to deliver the value your users came for. A professional UX audit provides that assessment quickly, rigorously, and with a clear path to improvement.

Your users made a brave decision when they trusted you with their financial lives. How you design their experience is your answer to that trust.

Frequently Asked Questions

1. What is FinTech app user retention?

FinTech app user retention refers to the percentage of users who continue using a financial application over a specific period after initial signup.

2. Why is retention important for FinTech companies?

Retention increases customer lifetime value, lowers acquisition costs, improves profitability, and drives sustainable growth.

3. What is the most common UX reason users churn from FinTech apps?

The most common UX-driven churn causes are a friction-heavy or incomplete onboarding experience that prevents users from reaching their first moment of value, poor dashboard usability that makes it difficult to access the information users care about, and irrelevant notifications that erode trust and goodwill. In most FinTech products, these three areas account for 60 to 70% of identifiable UX-driven churn.

4. How long does a FinTech UX audit take?

A comprehensive FinTech UX audit typically requires two to four weeks, depending on the scope and complexity of the product. This typically includes heuristic evaluation, user flow analysis, competitive benchmarking, and a prioritized recommendations report. Some agencies offer accelerated audit formats for early-stage products that can be completed in five to seven business days.

Share this blog!

Latest Blogs

Explore our latest insights on design, AI, and digital innovation.